公開日時 : 2020年08月04日

更新日時 : 2022年03月04日

Income Tax

As international talent works at Japan, they have to pay income tax annually .For Japan, the Tax year accounting period is form January 1 to December 31.

Foreigners who are leaving Japan before tax deadline must file their returns( On these dates February 16 to March 15 ) before thy leave, or designate a proxy to file a return for them .

Income tax is only required on income over 380,000 yen.

Hence, it could be understood that for all the tax payers who earn less than 380,000 yen could have filled a basic exemption which is meant to for your daily life expenses. This 380,000 yen is a basic exemption for all taxpayers including foreign workers who work in Japan.

Japan’s income tax law classified individual into three categories which is not related to visa types :

Resident

Permanent Resident: Foreigners who have Japanese nationality or who have an address and residence in Japan for at least 5 years, for the past 10 years.

Non-permanent Resident: Foreigners who do not have a Japanese nationality,Foreigners with total of 5 years or less who have had an address and residence in the past 10 years. Foreigners who are not “non-residents”.

Non-Resident

Foreigners who do not have an address in Japan or who do not have a residence in Japan for more than 1 year.

日本に住んでいる外国人の所得税について

外国人でも日本で働いていると「日本の税金」を支払うひつようがあります。税金に関する知識が無いと、払いすぎてしまったり、支払いを忘れて、遅れた分のお金をとられることもありますので、今回は所得税について紹介します。

所得税とは?

所得税は、お金を稼いだら支払う税金です。毎年1月1日から12月31日までに得たお金が課税(税金がかかる)されます。会社員やアルバイトをしている人などの労働者の人は、1年間に稼いだお金が103万円以上であれば所得税が発生します。1年間の所得が38万円以内であれば基礎控除(稼いだお金の中で、税金がかからないお金。だれでも受けることできます)の範囲内ですので、税務署に申告する必要もありませんが、それより多く収入があると税務署に申告しなければなりません。所得税は働いた人の所得に応じてかかりますが、外国人の所得税の扱いは居住者と非居住者で大きく違います。

居住者

居住者とは、日本に住所を持っている人、日本に1年上住んでいる人です。永住者と非永住者に分けられます。

永住者:日本国籍を持っている。または、外国人で過去10年以内に日本に住所があった期間の合計が5年以上。

非永住者:日本国籍を持っていない外国人で、過去10年以内に日本に住所があった期間の合計が5年以下。

非居住者

日本に住所を持っていない外国人で日本に1年以上居所(一時的に住んでいる場所)を持っていない人です。

Foreign employees need to know which of the following categories they belong to as the taxable range varies depending on the classification.

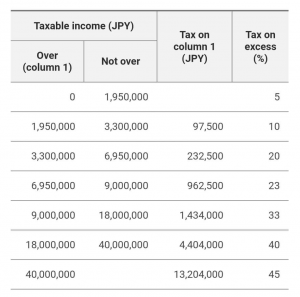

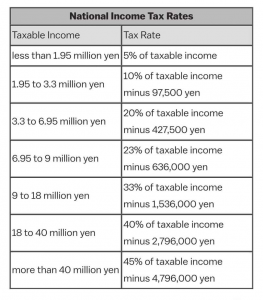

As for 1st of August 2020 income tax rate:

Foreign Tax Deduction

In order to avoid the issue of “ double tax payment ”, which indicates foreign residents who work in Japan have to pay both taxes in their home country and Japan.

According to the “OECD tax treaty “ which is an international standard, and serves as a model for concluding a tax treaty centered on OECD member countries. Japan, which is a member of the OECD, has adopted rules that are in line with this.

In short, the foreign income exemption method or foreign tax credit method is enforced in Japan.It is crucial for international workers who work in Japan to know that they have to check whether their country have the “OECD tax treaty” to avoid paying double tax to both countries.

二重払の防止について

日本で働いている外国人の中には、日本と母国の両方から税金がかかってしまう可能性があります。その対策として租税条約があります。これは税金を2つの国で二重に払うことを防ぐための条約です。

租税条約による手続きは、非居住者が受けられます。

租税条約に基づいて所得税の軽減や減税を受ける場合はには「租税条約に関する届出書」を提出します。

なお、払う税金の額はあくまでも参考です。その人の状況によって変わりますので、困ったら、専門家の人や税務署の職員の人に相談しましょう。

届出書はこちらから→国税庁「租税条約に関する届出書」

参考一覧:国税庁「2019 INCOME TAX AND SPECIAL INCOME TAX FOR RECONSTRUCTION GUIDE」、「所得税の税率」

財務省「租税条約に関する資料」、